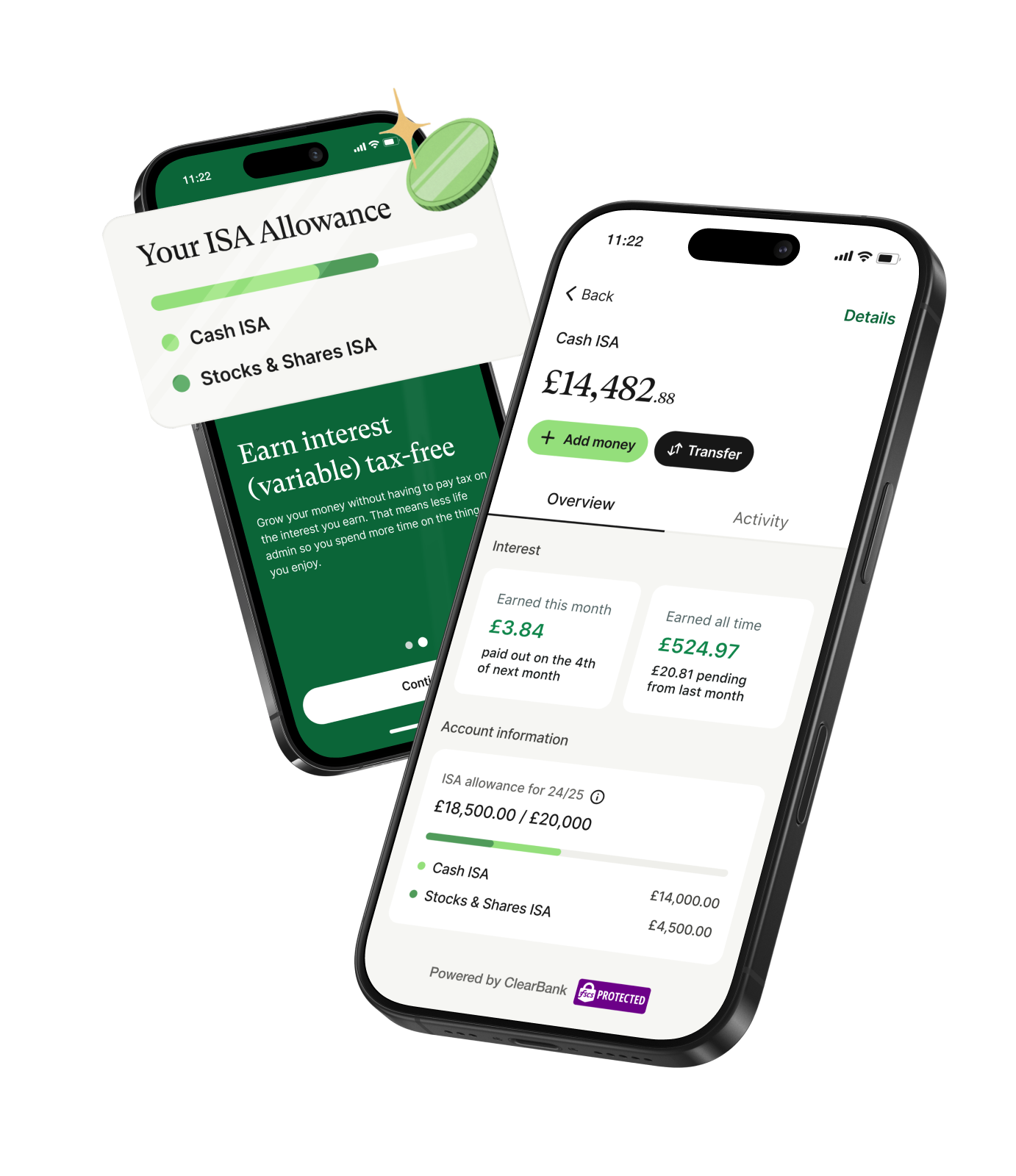

Earn 3.81% AER

We’re giving new customers the chance to earn a higher interest rate of 3.81% AER (variable tracker) on their Cash ISA for their first 12 months with the account.

Simply open a Chip Cash ISA, and we'll apply a 0.26% AER boost for 12 months on top of the standard rate of 3.55% AER (variable tracker).

This offer is for new customers only, see more information in the Chip Cash ISA Summary Box.

We’re giving new customers the chance to earn a higher interest rate of 3.81% AER (variable tracker) tax free on savings up to for 12 months with the Chip Cash ISA. Any amount over will earn the standard rate of 3.55% AER (variable tracker) during this period.

Simply open a Chip Cash ISA and we’ll apply the 0.26% AER boost to savings up to . After 12 months, all savings will earn the standard rate of 3.55% (variable tracker)

This offer is for new customers only, see more information in the Chip Cash ISA Summary Box.

Please note: This promotion cannot be used in conjunction with any other Boosted Rate Promotion. Only one promotional rate can be applied to your Chip Cash ISA account at any one time.

To be eligible for the Boosted Cash ISA Promotional Rate you must be a new Chip customer. A new customer is defined as someone who has never previously transacted in a Chip account and has no other promotional rates applied on any Chip products.

.avif)

.png)

.avif)