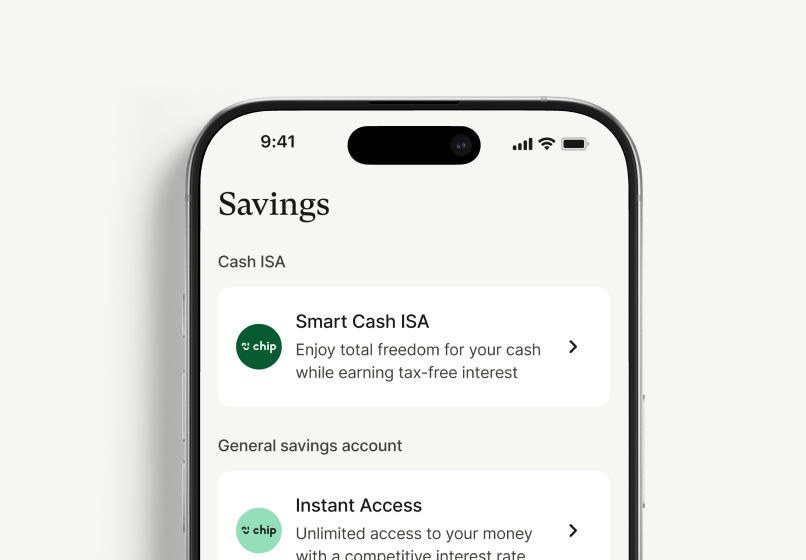

Our savings accountsView all

Smart Cash ISA

Our brand-new flexible cash ISA.

Prize Savings Account

Savings account with a monthly prize draw.

Instant Access

Highly competitive rates without withdrawal restrictions.

Easy Access

Easy access with instant deposits and withdrawals.

Cash ISA

Build your wealth with tax-free interest.

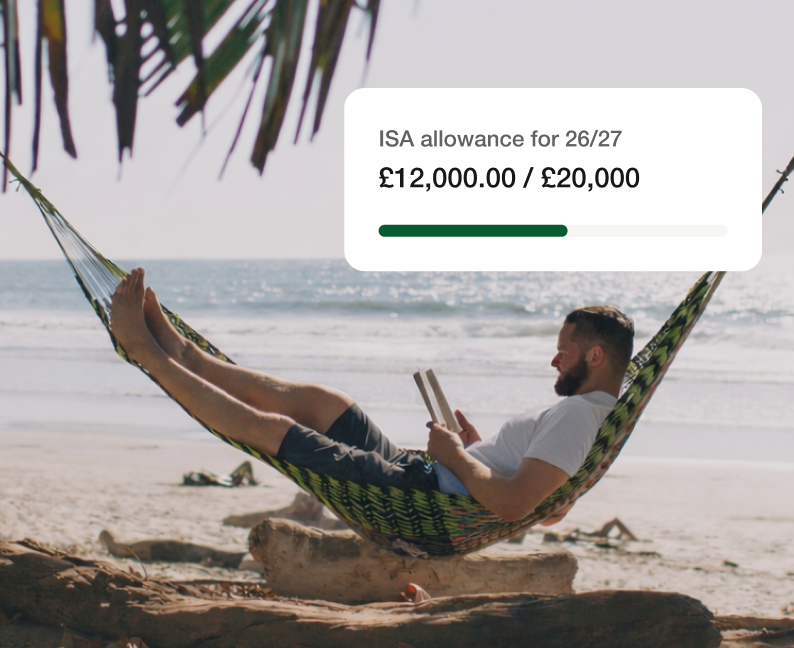

Our brand new Smart Cash ISA

Make the most of your £20,000 ISA allowance and earn interest tax-free1

Learn more

T&Cs apply, 18+ UK tax resident & app only.

The Smart Cash ISA is provided by Chip Financial (Investments) Ltd. ISA limits apply. Deposit up to £20k this tax year.

1Chip does not provide tax advice. Tax treatment depends on individual circumstances and may be subject to change in the future.

1Chip does not provide tax advice. Tax treatment depends on individual circumstances and may be subject to change in the future.

Other Funds 2

x

FTSE All-world

HSBC FTSE All-World Index Fund Accumulation C GBP

Semiconductor Fund

Invesco Physical Silver ETC USD

S&P 500 Tech

Vanguard S&P 500 UCITS ETF USD Acc

AI Fund

WisdomTree Artificial Intelligence UCITS ETF USD Acc

NASDAQ 100

iShares NASDAQ 100 UCITS ETF USD Acc

MSCI World

iShares Core MSCI World UCITS ETF USD Acc

China Fund

HSBC MSCI China UCITS ETF USD Acc

our Investing accountsView all

Stocks & Shares ISA

A popular and tax-efficient way to invest.

SIPP

Take control of your pension with flexible investing.

Invest in funds

Funds from the world’s largest asset managers.

All our investment funds

See the funds offered with Chip.

Our Investment FundsView all

.avif)

S&P 500

Vanguard S&P 500 UCITS ETF USD Acc

Physical gold

Invesco Physical Gold ETC USD

Space innovators

VanEck Space Innovators UCITS ETF A USD Acc

FTSE 100

Vanguard FTSE 100 Index Unit Trust GBP Acc

Other funds

When investing, your capital is at risk.

Invest with a Stocks and Shares ISA.

Make the most of your £20,000 ISA allowance and keep all of your returns1.

Learn more

With investments, you capital is at risk.

Seccl Custody Limited is the ISA Manager for the Chip Stocks & Shares ISA. Fund management charges apply. ISA limits apply. Invest £20k per tax year.

1Chip does not provide tax advice. Tax treatment depends on individual circumstances and may be subject to change in the future.

1Chip does not provide tax advice. Tax treatment depends on individual circumstances and may be subject to change in the future.

Register your interest for a Chip Pension.

The Self-Invested Personal Pension (SIPP) that knows when you want to retire. With LifePath funds managed by BlackRock. Built around you.

Learn more

With investments, you capital is at risk.

The Chip Personal Pension is provided by Chip Financial (Investments) Ltd.

When you pay into a personal pension, your money is usually invested in stocks and shares. The value of these investments can rise or fall, so you might get back less than you put in. Returns aren’t guaranteed.

Pension tax rules may also change in the future, and any tax benefits you receive will depend on your individual circumstances.

When you pay into a personal pension, your money is usually invested in stocks and shares. The value of these investments can rise or fall, so you might get back less than you put in. Returns aren’t guaranteed.

Pension tax rules may also change in the future, and any tax benefits you receive will depend on your individual circumstances.

Other Funds

x

FTSE All-world

HSBC FTSE All-World Index Fund Accumulation C GBP

Semiconductor Fund

Invesco Physical Silver ETC USD

S&P 500 Tech

Vanguard S&P 500 UCITS ETF USD Acc

AI Fund

WisdomTree Artificial Intelligence UCITS ETF USD Acc

NASDAQ 100

iShares NASDAQ 100 UCITS ETF USD Acc

MSCI World

iShares Core MSCI World UCITS ETF USD Acc

China Fund

HSBC MSCI China UCITS ETF USD Acc

Explore

Financial Tools

Calculators and planning tools

Investment Guides

Learn about investing

Savings Guides

Maximize your savings

Savings Guides

Maximize your savings

Financial Tools

Calculators and planning tools

Investment Guides

Learn about investing

Savings Guides

Maximise your savings

Pensions Guides

Learn about pensions

Featured insights

The what's of investingThe biggest companies by market capThe 'What's' of investing

The biggest companies by market cap

Learn about investing

Chip Investing Guides

Build your knowledge with our library of resources. Search our guides to understand the fundamentals of investing.

Learn more

When investing,

your capital is at risk.

your capital is at risk.

Financial Tools

x

investment guides

x

savings guides

x

Pensions Guides

x

The 'What's' of investing

x

The biggest companies by market cap

x

Explore

Fraud Protection

Keep your account secure

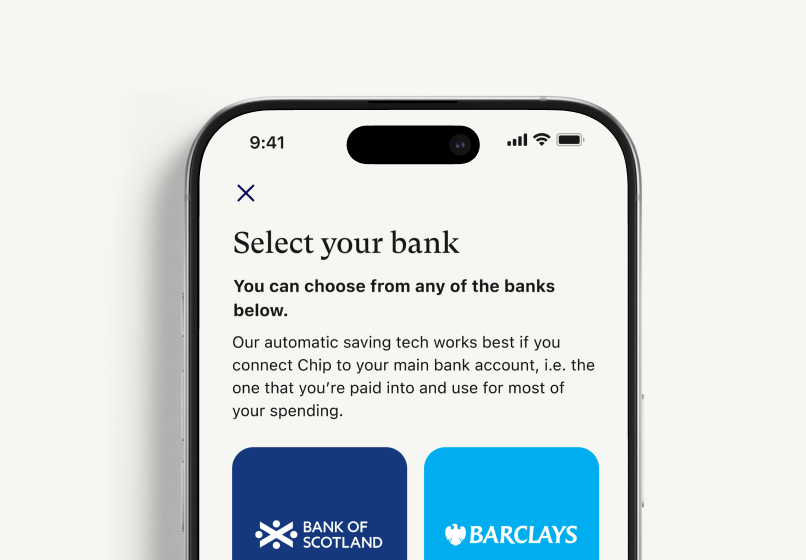

Change Bank Account

Update your linked account

How to connect your card

Link your card in minutes

How we use open banking

How we use your data securely

Support & reasonable adjustments

Support tailored to your needs

Further support

More ways to get support

Further support

More ways to get support

Ready-to-go answers

Need a hand?

We can help.

We can help.

Find quick answers to your questions and detailed guides on making the most of Chip in our Help Centre.

Visit Help Centre

further-support

x

Get the Chip App

Scan the QR code to download the app.

or get a download link via email.

Your download link is in your inbox. Install the app, create your account, and start building wealth!

Oops! Something went wrong while submitting the form.