.avif)

The pension that knows when you want to retire.

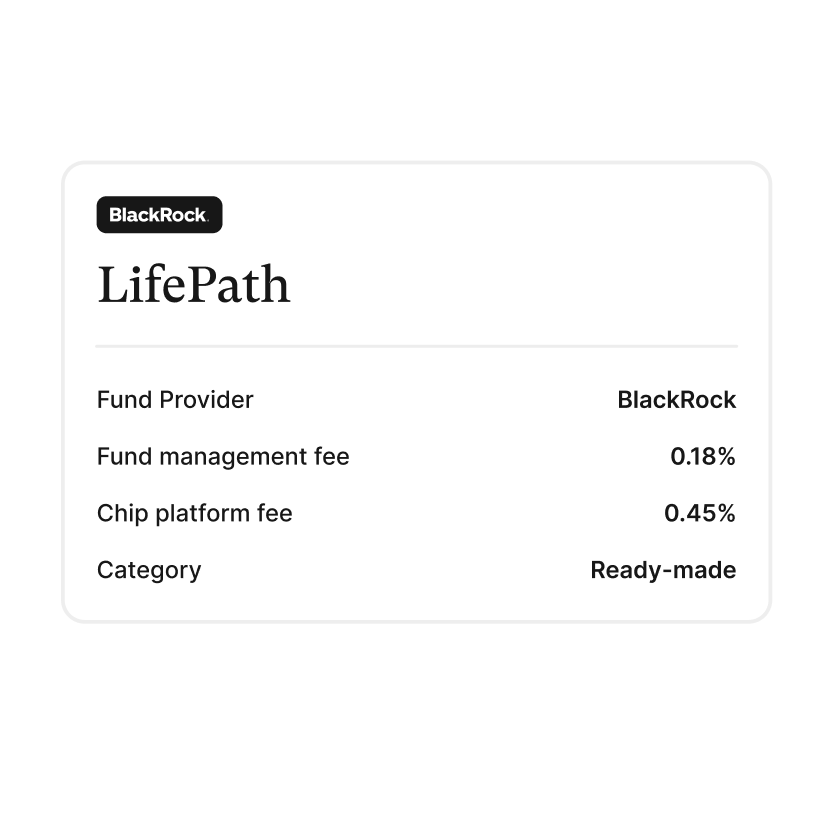

With LifePath funds managed by BlackRock. Built around you.

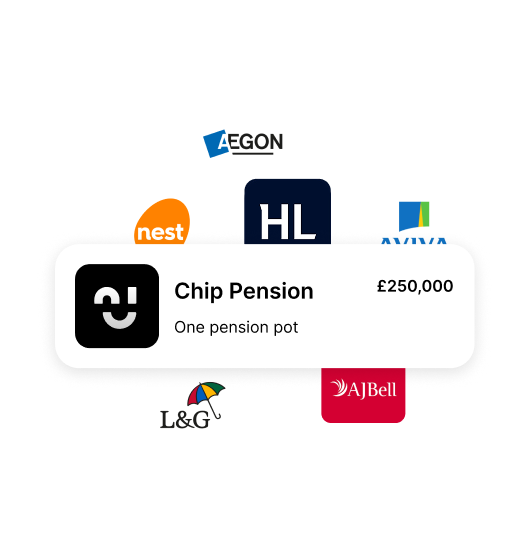

Most of us have pensions from old jobs, invested in who knows what, and who knows where. But we can change that. With Chip's personal pension, we’re making it simple to bring them all here, invested in one fund that’s set to your retirement age1.

1Before you transfer a pension, you should check for safeguarded and/or valuable benefits such as Guaranteed Annuity Rate, loyalty bonuses, or protected tax free cash you could lose as well as exit fees and investment choices.

If you’re unsure if a pension transfer is right for you, we recommend you speak to a financial adviser. They can give you personalised advice and recommendations to match your individual needs.

Currently, the Chip Personal Pension does not offer a drawdown option. If you would like to access your pension, you can transfer it to a provider that offers drawdown services.

The perfect companion for your workplace pension

While your current workplace pension does its thing, give us a few details of your old pension pots and we’ll get them working too. We handle the transfer process for you, with updates every step of the way.

Our Personal Pension

We’re putting the final touches to our SIPP (Self-Invested Personal Pension), so you can grow all your wealth in one place.

Tailored to your retirement age

Simple in-app setup

25% tax top up2

2Pension tax rules may also change in the future, and any tax benefits you receive will depend on your individual circumstances.

What are your old pensions costing you?

See how you could benefit by bringing your retirement wealth into one place.

Transparent fees

Transparent fees Your investment

Your investment App & user experience

App & user experience All your money in one place

All your money in one place Planning tools

Planning tools Customer experience

Customer experienceChip Pension

0.63% - Simple easy to understand fees consisting of your platform and fund management fee

Old Workplace Pension

Typically 0.20% to 1% but often with extra policy, admin, FX and contribution fees. Pension fees can vary, check with your provider for charges that might apply.

Chip Pension

One professionally managed fund, BlackRock LifePath Target Date Fund, which automatically rebalances as you approach retirement.

Old Workplace Pension

Auto-enrolled default fund. Often unchanged since you left the employer, may no longer suit your age, goals or risk profile.

Chip Pension

Modern mobile app — check your balance and manage your account in seconds

Old Workplace Pension

Many deferred pots sit in web portals originally built for active employees and require paper statements.

Chip Pension

Pension sits alongside savings, Cash ISA, Stocks & Shares ISA, GIA and prize savings — one login, one view of your wealth.

Old Workplace Pension

Pension only. A separate login (per old employer) and nothing else.

Chip Pension

AI Wealth Plan (coming soon) — personalised goals and progress tracking.

Old Workplace Pension

Most provide a basic retirement projection; very few offer active planning or AI-led guidance.

Chip Pension

Chip is rated 4.4★ 'Excellent' on Trustpilot (4,462 reviews). UK-based support 7 days a week.

Old Workplace Pension

Some large legacy providers have been known to impose additional barriers, including mandatory phone calls, duplicated forms and repeated identity checks to manage your pension.

When you pay into a personal pension, your money is usually invested in stocks and shares. The value of these investments can rise or fall, so you might get back less than you put in. Returns aren’t guaranteed. Pension tax rules may also change in the future, and any tax benefits you receive will depend on your individual circumstances.

How does it work?

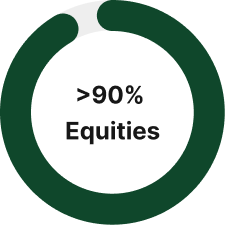

It removes the guesswork by rebalancing itself for you, helping your risk levels stay appropriate for your age without you ever having to lift a finger.

Chip does not provide financial advice, if you’re unsure what pension options are right for you, speak to a regulated financial adviser.

Early career

Halfway

At retirement

Source: BlackRock, as of 30 June 2023. For illustrative purposes only. Risk: Diversification and asset allocation may not fully protect you from market risk. Risk: While proprietary technology platforms may help manage risk, risk cannot be eliminated. *Early career“ (refers to starting point of 2065 fund) illustrates the intended equity allocation 40 years before the target date. "Halfway" illustrates the intended equity allocation 20 years before the target date. "Retirement" illustrates the intended equity allocation at the target date. Asset allocations may periodically be adjusted based on an assessment of current market conditions. See the funds' prospectus for more information on each fund’s intended asset allocation mix over time. The principal value of the funds is not guaranteed at any time, including at the target date

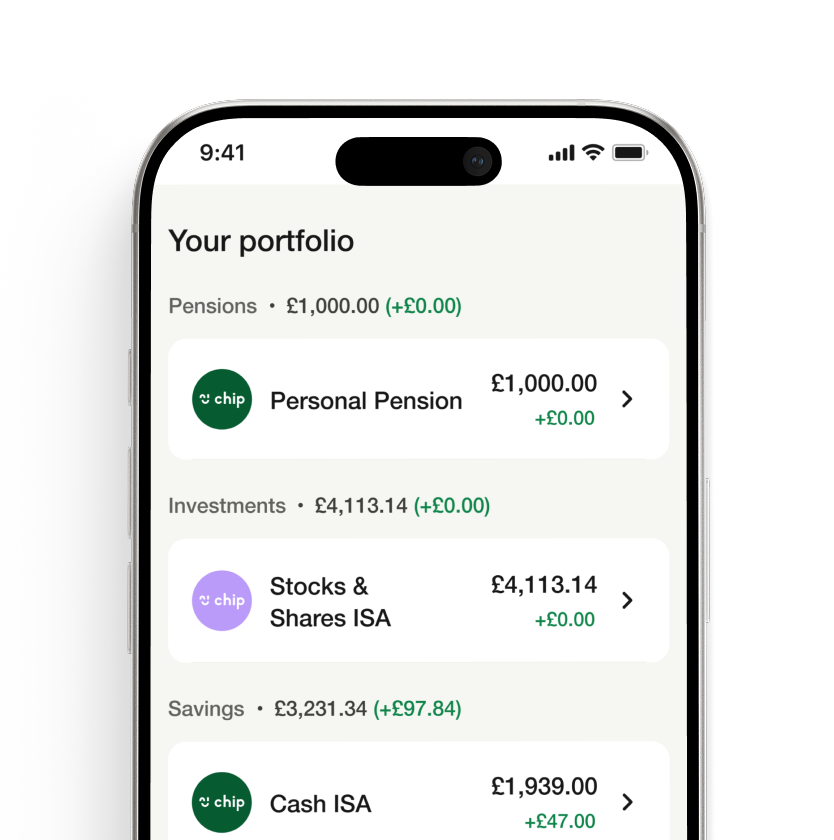

Savings, Investments & Pensions, all in one place

Transparent fees

We’re here for you, seven days a week

Transfers are coming soon...

We’re working on making it super easy to transfer your existing pensions to Chip. Register your interest and we’ll let you know as soon as transfers are available.

Pre-register to be first to know

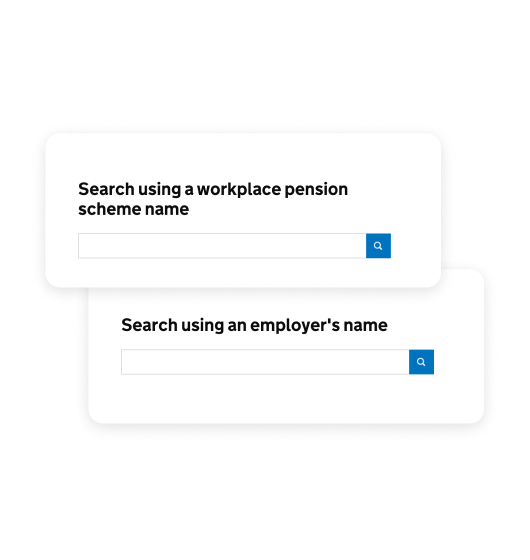

How to find your lost pensions

The average person has 11 jobs in their lifetime, which could mean 11 different pension pots scattered across different providers, with potentially high fees that can really add up. The government’s free pension tracking service can help you find them.

Go to the free Pension Tracing Service at gov.uk

Find the names of your old employers or pension providers

Interested in transferring to Chip? Register your interest

How to open your account

We've made it easy to get started. Open your account in just a few minutes.

Better rates, same protection

Trusted by over 400,000 people.

FSCS protected up to £85,000

Your SIPP is operated by Chip Financial (Investments) Ltd, and your investments are held by Seccl Technology Limited as custodian. Both firms are authorised and regulated by the FCA.

If either firm were to fail and there was a shortfall in the assets they hold on your behalf, you may be entitled to compensation from the financial services compensation scheme (fscs) of up to £85,000 per eligible claimant.

BlackRock acts as the investment manager for the underlying funds. FSCS protection does not cover investment losses resulting from market movements or fund performance. FSCS protection applies only in limited circumstances relating to firm failure or mismanagement, not normal investment risk.

Protect yourself with biometrics

Protection for your mobile device with biometric login. As an additional security layer all Chip users need to create a 6-digit PIN to access their app.

Bank-level encryption

Every connection to Chip is secured with bank-grade encryption and built on Open Banking technology – the regulated standard for seamlessly linking accounts.

We’ve got your back

Our systems continuously monitor for suspicious activity, helping keep your account protected from fraudsters.

Help when you need it

Our UK-based customer support team is just a message away, ready to help whenever you need it.

Any questions about our SIPP?

For every eligible contribution you make the government applies tax relief at 20% gross. This equates to a net 25% top up of your pension.

Example: You pay in £800, and the government adds £200, giving you a total of £1,000 in your pot instantly.

If you’re a higher or additional-rate taxpayer, you can usually claim back an additional 20-25% through your Self Assessment tax return.

Absolutely. Most of us have pension pots from previous jobs that may not be right for us, often with high fees. With Chip, you’ll be able to bring all those old pots into one place so you can track your total retirement wealth in the app alongside your other savings.

Yes. You can have as many SIPPs as you like. You can use a SIPP alongside your workplace pension to have more control over your total retirement strategy. The only thing to remember is stay within your annual allowance (generally the lower of 100% of your earnings or £60,000).

Chip Financial (Investments) Ltd is authorised and regulated by the Financial Conduct Authority. All your cash and investments are held by our regulated partner custodians. Additionally, like all our investment products, your pension assets are protected by the Financial Services Compensation Scheme (up to £85,000) should a firm fail, subject to eligibility.