- The RBS Instant Access ISA currently offers two rates; for balances less than £24,999, the rate is 1.15% AER/tax-free. For balances above £24,999 the rate is 2.45% AER/tax-free.

- Interest on this account is paid annually.

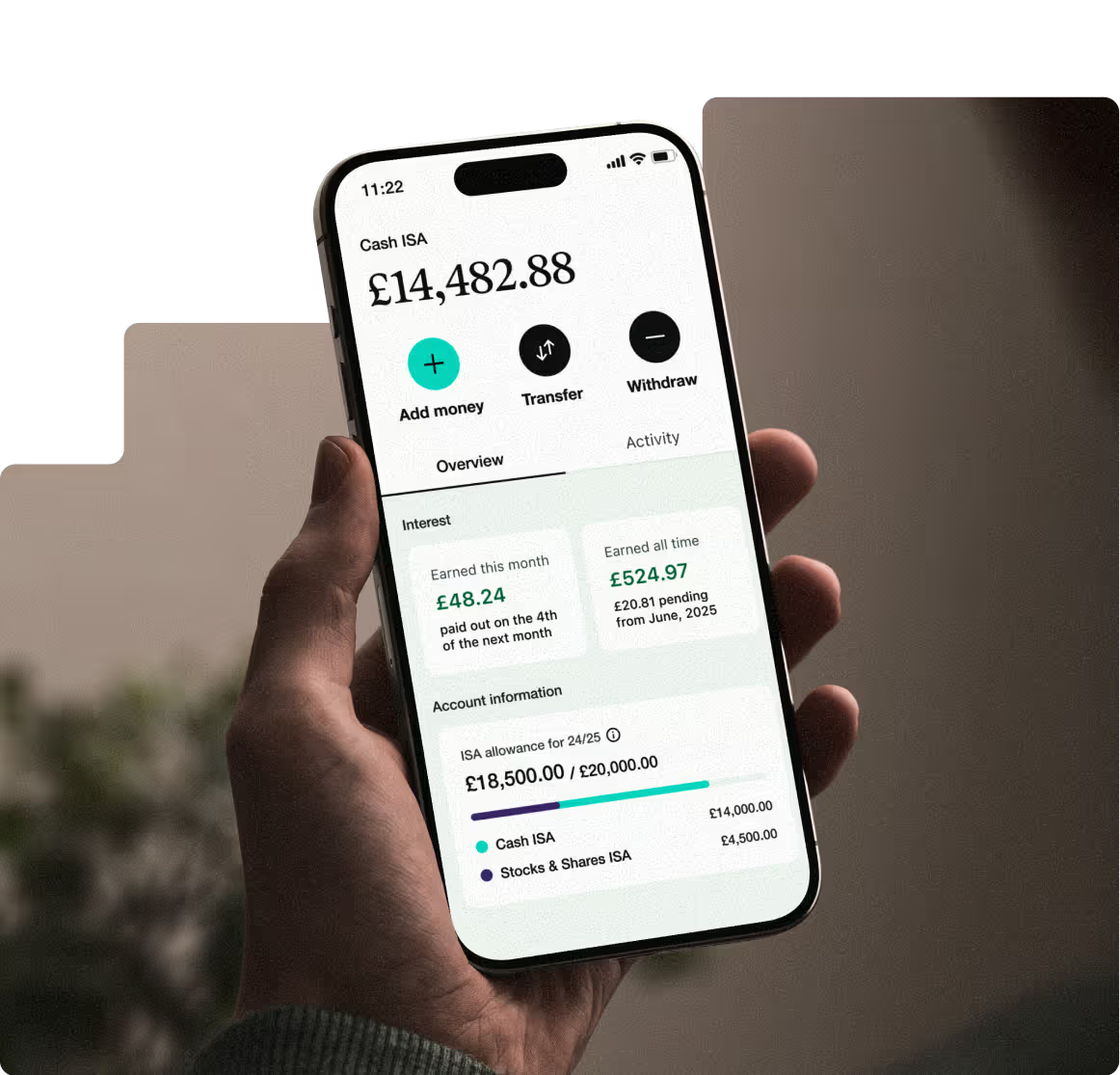

- You can open a RBS Instant Access ISA from £1 and can withdraw money from this account at any time with no penalty. You can get a higher rate from £25,000+.

What is an instant

Cash ISA?

What is an Instant Cash ISA?

An Instant Cash ISA is a UK savings account where your interest is tax-free, and you can access your money instantly without paying any penalties.

Is this account it right for me?

A Cash ISA is a great choice if you want a flexible way to grow your savings while making the most of your annual tax-free allowance.

How to research and compare Cash ISA accounts

Tips for comparing Cash ISAs

The right Cash ISA should match your savings style while helping you make the most of your tax-free allowance. Here are some things to keep in mind:

Don’t just stick to high street banks. Online banks, building societies, and fintech apps often offer better rates. Compare their accessibility, features, and interest options.

Even “instant access” ISAs may have limits on withdrawals or minimum deposit rules. Always check the fine print, as withdrawing funds can affect your annual ISA allowance.

Introductory or bonus rates can be attractive, but they don’t last forever. Pay close attention to how long the promotion runs and what the standard rate will be afterward.

Financial calculators can help you see how your savings might grow. Try our Interest Rate Calculator to test different deposit amounts and rates.

Is it worth having a Cash ISA?

An instant Cash ISA can be a smart way to grow your savings while keeping them accessible. But, like any other financial product, it’s worth weighing up the benefits and drawbacks before you decide.

Advantages

Tax-free growth:

All the interest you earn is free from UK income tax, helping your savings build more quickly and efficiently over time.2

Instant access:

Many accounts let you withdraw money straight away without penalties, perfect for unexpected expenses or changing goals.

Flexible saving:

Choose how you save: make regular deposits or add lump sums whenever it suits you.

Plenty of choice:

From high street banks to app-based fintechs, you’ll find a wide range of accounts with competitive rates, features, and accessibility.

Disadvantages

Typically lower rates:

Instant Cash ISAs often pay less interest than fixed-rate or notice accounts because they prioritise flexibility and immediate access to funds.

Annual contribution limits:

You can only save up to the annual ISA allowance (£20,000 for 2025/26), which may be restrictive if you want to deposit a large sum in one go.

Possible withdrawal limits:

Some accounts cap the number of withdrawals or reduce your interest rate if you dip into your savings too often.

Variable returns:

Rates can change at any time, meaning your earnings may rise or fall.

People also ask

Common Cash ISA questions

With competitive rates now available, it can be just as rewarding as other savings accounts while protecting you from future tax changes. It’s a simple, secure way to make the most of your money.

They remain a popular, government-backed way to save tax-free, and current proposals only look at adjusting allowances, not removing them. For savers, they’re still a secure and future-proof option.