- The Santander Easy Access ISA currently offers a rate of 2.00% AER (variable) for 12 months.

- Interest on this account is paid annually.

- You can open a Santander Easy Access ISA from £500 and can withdraw money from this account at any time with no penalty.

- After 12 months, your account is transferred to an ISA Saver.

What is an instant

Cash ISA?

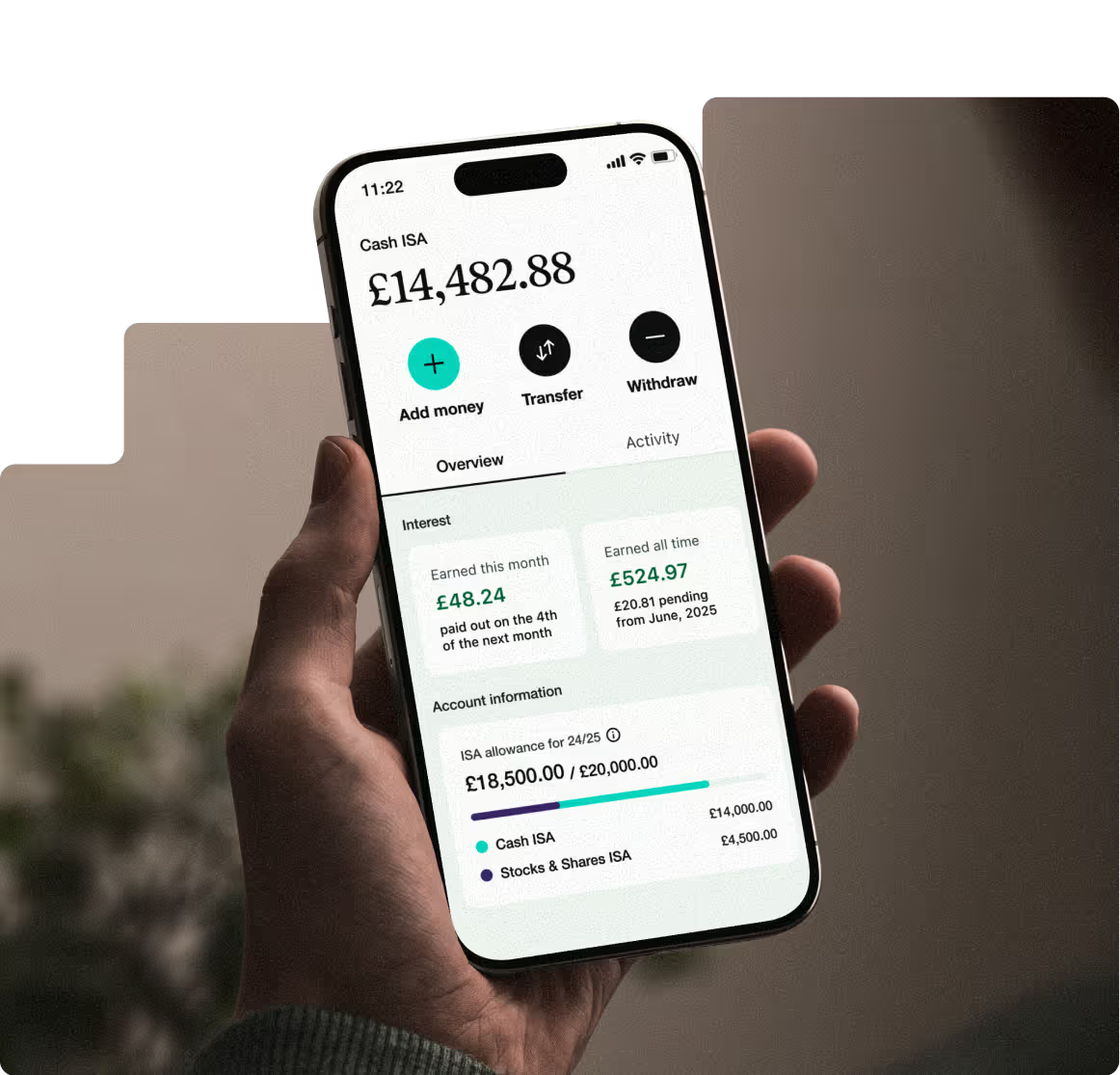

What is an Instant Cash ISA?

An Instant Cash ISA is a savings account where you earn interest on your money without paying tax on it, while still being able to access your funds freely whenever you need them.

Is this account it right for me?

A Cash ISA could be the perfect choice if you're looking for a flexible way to save and want to maximise your tax-free allowance.

How to research and compare Cash ISA accounts

Tips for comparing Cash ISAs

The right Cash ISA should match your savings style while helping you make the most of your tax-free allowance. Here are some things to keep in mind:

Don't just stick to high street banks. Online banks, building societies, and app-based providers, like Chip, often offer more competitive rates. Compare interest rates, account features, and access options, whether it's via an app, online banking, or in-branch.

Even with 'instant access,' some ISAs may have restrictions on withdrawals, minimum deposits, or when interest is paid. Always read the terms carefully. Remember, withdrawing funds could affect your annual ISA allowance, so know the potential impact before you take money out.

Some providers offer an introductory rate to attract new savers. While a higher rate is appealing, check how long it lasts and what the standard rate is afterward. Evaluate the long-term viability of the account beyond the initial bonus.

There are a variety of online financial tools that can help you quickly understand the rate of your returns. Use our Interest rates calculator to see how your money could grow over time based on interest rates, deposits, and length of time.

Is it worth having a Cash ISA?

An instant Cash ISA can be a smart way to grow your savings while keeping them accessible. But, like any other financial product, it’s worth weighing up the benefits and drawbacks before you decide.

Advantages

Tax-free growth:

Any interest you earn is free from UK income tax, which helps your savings grow faster and more efficiently2.

Flexible access to your savings:

Many accounts offer instant, penalty-free access to your funds, providing you with the flexibility you need for unexpected costs.

Save your way:

You can save at your own pace. Many providers let you deposit regular amounts or large lump sums, giving you complete control over your savings plan.

Wide choice of providers:

You aren't limited to one type of bank. High street, online, and app-based providers all offer competitive rates and features, so you can shop around for the best fit.

Disadvantages

Lower interest rates:

Instant Cash ISAs typically offer lower interest rates compared to fixed-rate or notice accounts, as they provide more flexibility to access your cash.

Annual allowance limits:

Your deposits are limited to the annual ISA allowance (£20,000 for 2025/26), which can be a restriction for those with larger savings.

Possible withdrawal restrictions:

Some accounts may limit the number of withdrawals or lower your interest rate if you take money out too often. Always check the terms carefully.

Variable rates:

Interest rates on these accounts can change at any time, which means your returns could go up or down.

People also ask

Common Cash ISA questions

With competitive rates now available, it can be just as rewarding as other savings accounts while protecting you from future tax changes. It’s a simple, secure way to make the most of your money.

They remain a popular, government-backed way to save tax-free, and current proposals only look at adjusting allowances, not removing them. For savers, they’re still a secure and future-proof option.